2023 Letter - Mexican Investor

Portfolio holdings, returns and learnings.

After a 2021/2022 with high inflation and aggressive interest rate hikes in 2022, the general consensus was that all of this would lead to a recession and a market crash this year. However, once again, it was confirmed that in life and in the stock market, no one knows what is going to happen.

That’s why it’s so important to always stay invested, because if this year you had decided to stay in cash waiting for a correction, you would have missed out on a year of 20-25% returns on average, according to the performance of various indexes and portfolios from people I follow on Twitter. And the most important thing to remember is that even if there is fear in the market, if the valuations of companies are attractive, sooner or later the price will adjust to a more reasonable valuation, and if you don’t buy, by the time you realize this, it will already be too late.

For 2024, the outlook is completely different. With inflation now around the average of the last 20 years and the economy remaining solid, the U.S. Federal Reserve has already begun signaling that they will start lowering interest rates or, at the very least, keeping them steady. This will stimulate the economy, credit will return, and it should mark the beginning of another bull market, especially now that we’re starting from a base of low valuations and after the excess liquidity in the system, which had been caused by the chaos of the COVID-19 pandemic, has been cleared.

Last year I learned an important lesson, and this year I want to remind myself once again of a phrase I mentioned during my 2022 annual letter:

"I do what I believe the circumstances require of me. I have no preferences; having preferences would be having weaknesses."

— Magnus Carlsen

This year, I kept this phrase in mind constantly, and I made money in all kinds of investments and companies. From Polish small caps to U.S. large caps. Special situations or quality-growth investments. Whenever there was an interesting opportunity to make money with minimal risk, I took it.

Currently, I am completely agnostic to the size and type of companies I invest in because I don’t see the point in limiting myself to just one type of investment. I learned this the hard way last year, when I missed out on fantastic investment opportunities by focusing only on small caps. There’s nothing wrong with small caps, but there were also absolute bargains in well-known large companies like Meta, Adobe, or Amazon, which I regret not taking advantage of. In any case, lesson learned.

This follows the line of thinking of two of my favorite investors in history: Peter Lynch and Joel Greenblatt. Greenblatt even has a book dedicated to investing in special situations, which between 1988 and 1994 helped him achieve annual returns of 30% after taxes and fees. On the other hand, Lynch used to divide his portfolio into six categories, diversifying into investments he called “slow growth,” “fast growth,” “core holdings,” “cyclical,” “turnarounds,” and “asset plays.”

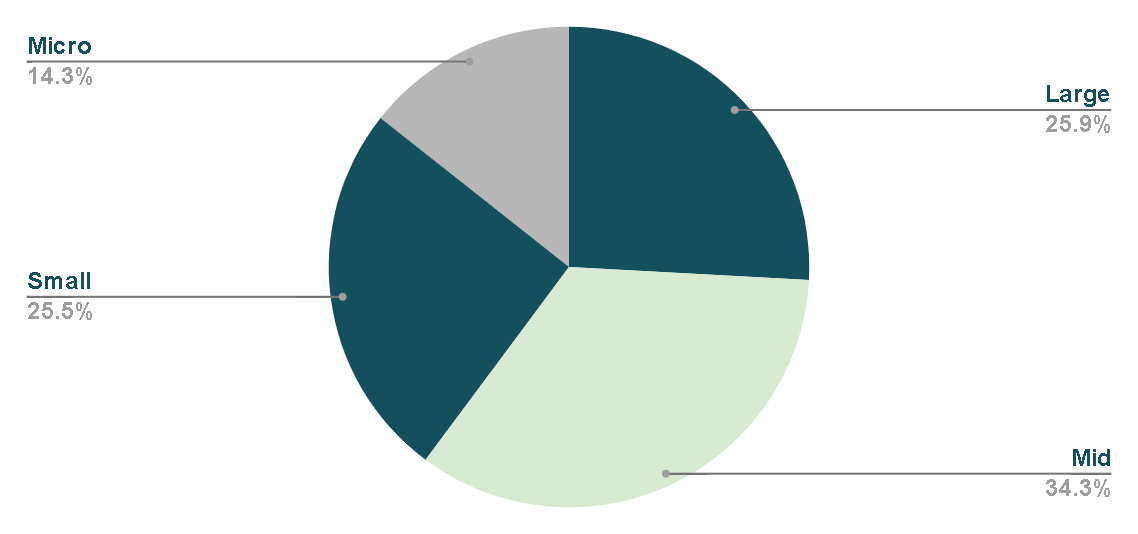

This year, my portfolio is fairly diversified by size: 25% is in large companies, 34% in medium-sized companies, and the rest in small ones. Additionally, 20% of the portfolio is in what I call ‘Special Situations and Value Investments.’ These are companies I am interested in holding for a shorter period or until a specific event occurs that moves the stock price.

There will be years of planting, where, even though we don’t see the fruits of the investment, the ground will be in perfect condition to start planting. There will also be years of harvesting what we’ve sown previously, where we won’t be able to buy as much, but we will see our capital grow, just like this current year. In all scenarios, there is a gain, and what matters is enjoying the process.

Current Portfolio

Below I will mention each of the positions that make up my portfolio, a brief pitch of why I’m invested and what I expect in the future, the weight percentage, performance and some key metrics to give you an idea of the quality of each one. If you are interested in reading more, I will also leave links to my analysis of each one.

AutoPartner

This is my largest position, not only due to the return I have achieved, but also because of the quality of the business and the confidence I have in its future.

As a regular user of AutoZone and O'Reilly, I understand how important auto parts businesses are. In the case of AutoPartner, I like the opportunity it has to become the leader in this sector in Eastern Europe, as there is currently no clear competitor dominating the market. If things don't change, this could be a company that stays with me for life.

Portfolio Percentage: 10.8%

Average Price: 18.66 PLN

Total Return: 39%

LTM PER: 15x

5-Year EPS Growth: 35%

LTM Net Margin: 6.45%

LTM ROCE: 26%

Sprouts Farmers

This is the company that has been in my portfolio the longest, since around the end of 2021, although I have bought and sold it several times over this period, mostly to take profits.

Sprouts is a supermarket chain focused on selling organic and healthy food, both private label and other brands. It is currently present in only 23 of the 50 U.S. states, so it has room to grow, and the management has developed a strategic plan to ensure growth occurs as smoothly as possible. You can read my in-depth article on the company on Seeking Alpha.

Portfolio Percentage: 10.5%

Average Price: $33.92 USD

Total Return: 42%

LTM Free Cash Flow Yield: 5.3%

5-Year Per Share Free Cash Flow Growth: 21%

LTM Free Cash Flow Margin: 3.95%

LTM Free Cash Flow ROCE: 10%

Ulta Beauty

This is one of the companies I have spent the most time understanding why it has been successful in the stock market, and I also have a very high conviction in it. This December, I visited their physical store a couple of times, and on all occasions, I found the stores absolutely packed.

Recently, the stock went through a dip, which I consider to be a market inefficiency driven by irrational fears about what a recession might do to its earnings. While the recession doesn't seem to be materializing, I think even if it did, the company would do well.

This is my analysis on Seeking Alpha.

Portfolio Percentage: 9.2%

Average Price: $392.53 USD

Total Return: 25%

LTM Free Cash Flow Yield: 4.1%

5-Year Per Share Free Cash Flow Growth: 13%

LTM Free Cash Flow Margin: 8.95%

LTM Free Cash Flow ROCE: 43%

SDI Group

This is the worst investment I've made in my life when considering the current performance and the poor analysis I made when purchasing it for the first time back in February 2022. Additionally, the opportunity cost has been significant.

For example, since my first purchase, the stock has dropped 45%. During this same period, similar companies (in terms of business model, not necessarily quality) have delivered returns such as +30% for Judges Scientific, -6% for Halma, and -5% for Danaher and Thermo Fisher. I just happened to buy the company in the sector that was going to perform the worst over the next 22 months!

Now, why do I keep the position? First, because I believe the business can recover from the problems it is facing. Second, because I don't plan to sell at the current valuation of 9x EBITDA and 13x Free Cash Flow. Lastly, because Warren Buffett haunts me at night, reminding me to be greedy when others are fearful.

I have felt tempted to sell and close the mistake I made by buying inflated earnings at a high valuation due to my inexperience, but I decided not to sell, nor to buy more. I will simply let the position recover eventually, if it does.

Portfolio Percentage: 9.1%

Average Price: £1.40 GBP

Total Return: -38%

LTM Free Cash Flow Yield: 7.4%

5-Year Per Share Free Cash Flow Growth: 22%

LTM Free Cash Flow Margin: 10%

LTM Free Cash Flow ROCE: 10%

I once wrote an article on Substack explaining the thesis and also went into detail about the temporary problems the company is facing on Seeking Alpha.

Fleetcor Technologies

Initially, my average price was $199 USD, but I sold it at $274 to realize a 38% gain, and then I bought it again when it dropped to $250. The company has a product that serves a critical mission for its clients, and its software for controlling purchase and payment processes related to employee travel expenses helps reduce the risk of fraud and improve expense control. That’s why, whether there’s a recession, inflation, or economic events, as long as there are employees spending company money, there will be demand for Fleetcor.

What I also like is that, even though their main product is software, a significant portion of the company's profits comes from long-term relationships with hotels, gas stations, travel agencies, and others. This way, the company can offer better promotions to clients, providing more added value. This is extremely important because if they only depended on technology, their product would be much more replaceable.

Here’s my analysis on Seeking Alpha.

Portfolio Percentage: 8.7%

Average Price: $249.72 USD

Total Return: 13%

LTM Free Cash Flow Yield: 5%

5-Year Per Share Free Cash Flow Growth: 14%

LTM Free Cash Flow Margin: 28.6%

LTM Free Cash Flow ROCE: 12%

Eurofins Scientific

Eurofins is a group of laboratories that provide testing services to industries such as pharmaceuticals, food, and consumer products. Just like many companies in the medical equipment and laboratory sector (SDI Group was also affected by this), during 2020, one-off contracts inflated earnings, and when these started to expire, the market realized it had gone too far in euphoria, swinging from greed to fear, creating investment opportunities in high-quality companies like Eurofins.

Currently, I don’t see it as attractive as when I bought it, but I really like the sector and will likely hold it for many years. Here's my analysis on Seeking Alpha.

Portfolio Percentage: 7.9%

Average Price: €48.2

Total Return: 22%

LTM Free Cash Flow Yield: 3.6%

5-Year Per Share Free Cash Flow Growth: 12%

LTM Free Cash Flow Margin: 6.4%

LTM Free Cash Flow ROCE: 10%

Bath & Body Works

I would categorize B&BW as the Ulta Beauty of fragrances. The company is basically a retailer of personal care products and home fragrances, such as perfumes, body lotions, shower gels, candles, and more.

Unlike Ulta, in B&BW stores, the vast majority of products are from their own brand, which is well recognized in the United States and Mexico. An important part of the thesis is that the brand has been built around a sensory experience in the store, allowing customers to smell various products before making a purchase. This is called sensory marketing, and it plays a big role in creating a brand and an experience that makes customers want to return frequently. It also reduces the risk of the brand being replaced by e-commerce, with customers opting to shop on Amazon, for instance.

Currently, it trades at a PER of 13, but when I bought it, it was at a PER of 11, which was an incredibly low valuation. You can read my article on Seeking Alpha.

Portfolio Percentage: 7.6%

Average Price: $35.25 USD

Total Return: 22%

LTM Free Cash Flow Yield: 8%

5-Year Per Share Free Cash Flow Growth: 5.5%

LTM Free Cash Flow Margin: 10.7%

LTM Free Cash Flow ROCE: 20%

Graphic Packaging

Graphic Packaging is a provider of packaging products, such as folding cartons, beverage containers, carton packaging, and flexible packaging solutions. These are sold to highly stable industries like food and beverage, consumer goods, and healthcare, making their revenue highly predictable and resistant to crises.

Currently, it can be purchased at a PER of 11x, so the margin of safety is considerable for a compounder. Here's my article on Seeking Alpha.

Portfolio Percentage: 6.6%

Average Price: $23.29 USD

Total Return: 6%

LTM PER: 11x

5-Year EPS Growth: 25%

LTM Net Margin: 7%

LTM ROCE: 15%

Corporativo Fragua

This company has a mix of pharmacy-type stores, like CVS or Walgreens, and convenience stores, which they call "Super Farmacias." Again, it’s a highly stable consumer business that is still growing, and according to various surveys, Farmacias Guadalajara (owned by Fragua) are among the top favorite pharmacies for Mexicans. It’s a solid business with strong brand power and growth, at a PER of 12x.

This is one of my candidates for expanding the position soon.

Portfolio Percentage: 6.5%

Average Price: 482 MXN

Total Return: 4%

LTM Free Cash Flow Yield: 8%

5-Year Per Share Free Cash Flow Growth: 53%

LTM Free Cash Flow Margin: 3.7%

LTM Free Cash Flow ROCE: 16%

Enghouse Systems

The company develops specialized software for specific industries. It also provides software for customer engagement and contact centers. While it's a decent business, what attracted me most when I bought it was the story behind it.

The company is transitioning its business model from perpetual licenses to Software as a Service, which will provide more recurring and predictable revenues. You can read the thesis on Seeking Alpha.

Portfolio Percentage: 5.6%

Average Price: $33.67 CAD

Total Return: 4%

LTM Free Cash Flow Yield: 6%

5-Year Per Share Free Cash Flow Growth: 4%

LTM Free Cash Flow Margin: 25%

LTM Free Cash Flow ROCE: 20%

The Italian Sea Group

This was the company I decided to buy to gain exposure to the luxury sector. Italian Sea Group manufactures yachts, some of which can reach up to 100 meters in length and cost several million dollars, so you can imagine the type of clients they attract.

This is precisely what led me to invest in the company, as yachts of this scale are only accessible to ultra-high-net-worth individuals (UHNWI), for whom recessions, inflation, and other economic issues hardly have any impact. Therefore, the company’s revenue can be much more resilient. Imagine Jeff Bezos being worried because inflation went from 3% to 5%, or Cristiano Ronaldo concerned about the Fed announcing a rate cut before he resumes spending. It simply doesn’t happen.

Portfolio Percentage: 5.2%

Average Price: €7.86

Total Return: 5%

LTM PER: 14x

5-Year EPS Growth: 128%

LTM Net Margin: 9%

LTM ROCE: 16%

Garrett Motion

Garrett Motion is the first company in the 'Special Situations and Value Investments' category. It’s a company that manufactures parts for automobiles, which caused the market to become fearful of potential revenue declines due to the expected recession, as well as the possible disappearance of the business due to the transition toward electric vehicles.

However, the company is one of the best in manufacturing turbocharging and electric propulsion solutions, so it will also be crucial for the development of electric vehicles. When I decided to buy, the company was trading at 6x EV/EBITDA, so just with the multiple rising to a more reasonable 8-10x (as it is now, trading at 8x), there was upside potential. If you added that they were expected to grow sales by 8% this year, you had a deep-value situation where the risk was minimal. Here’s my more detailed article on Seeking Alpha.

Portfolio Percentage: 4.7%

Average Price: $7.10 USD

Total Return: 36%

LTM Free Cash Flow Yield: 11%

5-Year Per Share Free Cash Flow Growth: 0%

LTM Free Cash Flow Margin: 10%

LTM Free Cash Flow ROCE: 35%

Dole

This is another company I've had in my portfolio since 2022, although I've sold it with profits a few times, and I plan to increase my position soon. It’s another special situation that emerged from the merger of Dole Food and Total Produce, which made Dole the undisputed leader in fruit and vegetable sales, along with vertical integration — owning 114,000 acres for planting and 16 vessels for transporting the product, which allows for better supply chain control and less vulnerability to inflation.

All of this makes the margin expansion opportunity quite interesting. Currently, the EBITDA margin is at 3%, but competitors like Fresh Del Monte have achieved margins of 7-8%, despite being a smaller player without Dole's vertical integration, so reaching 5-6% margins seems very feasible. This means there are three important profitability levers: low-single digit revenue growth, margin expansion, and multiple expansion. All of this is because the merger caused accounting to be unclear, and there are still synergies yet to be reflected in the numbers.

Here’s my more detailed article on Seeking Alpha.

Portfolio Percentage: 4.4%

Average Price: $11.68 USD

Total Return: 7%

LTM Free Cash Flow Yield: 14%

5-Year Free Cash Flow Growth: 55%

LTM Free Cash Flow Margin: 1.8%

LTM Free Cash Flow ROCE: 6%

Berry Global

This company is also a special situation in an absolutely defensive business.

Berry Global is in the business of selling plastic packaging products, similar to Graphic Packaging, in a stable sector. The special situation arose because the company had historically grown through acquisitions, which made sense as the market was quite fragmented. However, they ended up accumulating a lot of debt and sacrificing things like share buybacks during times when the valuation was low, or simply paying out dividends, considering they were no longer a high-growth company.

All of this changed with the arrival of activist investors, who forced a change in the CEO, leading to a complete shift in capital allocation. Now, 80% of the capital is generated from cash flow from the business, and it is being used to pay down debt, repurchase shares, and start paying dividends. And as the saying goes, a picture is worth a thousand words. Below, you can see the drastic change in capital allocation:

The idea here is that not only will we now be rewarded as shareholders through dividends and share buybacks, but this could also attract a base of shareholders drawn by these benefits. Considering that it is currently trading at a P/E ratio of 13 after a 20% increase, it seems the opportunity was reasonable. You can read my full article on Substack and my post-results update on Seeking Alpha.

Portfolio Percentage: 3%

Average Price: $56.93 USD

Total Return: 20%

LTM Free Cash Flow Yield: 11%

5-Year Per Share Free Cash Flow Growth: 9%

LTM Free Cash Flow Margin: 7%

LTM Free Cash Flow ROCE: 7%

In summary, this would be how my portfolio is structured:

Performance

Although you can already get an idea that it was a good year for the portfolio (I think it was a good year for everyone), I wanted to show the total weighted performance, because for a good part of the year my portfolio was divided between two brokers.

Edit (5/Nov/2024): Hi, I'm Gustavo from 2024. I recently managed to import the information from my two brokers into a platform called Portseido to calculate my exact returns. For this year the final return was 45%, compared to 24% for the S&P500 or 16% for the Russell 2000.

In conclusion, it was a good year and we have reason to think that the next one will be as well, but at the end of the day, the market is unpredictable and it is best to always be invested.

Edit (5/Nov/2024): I come from the future, yes 2024 was a indeed a good year too.

If you don't believe me, just go to Twitter at the beginning of the year, when everyone was predicting a severe recession and telling you it was better to sell or wait for the market to go down further. The famous "it's still early."

For my part, I’m quite happy with my current portfolio, the diversification and the peace of mind that the businesses I’m invested in give me. I hope it has been a good year for everyone too and thank you for reading me throughout 2023. See you in 2024, greetings and happy holidays!

Disclaimer

All content on this blog is for informational purposes only and under no circumstances, whether express or implied, shall be considered investment, legal or other advice. Please do your own research and due diligence.